Most people earning six figures still feel trapped paycheck to paycheck—here's the mathematical escape route they're missing.

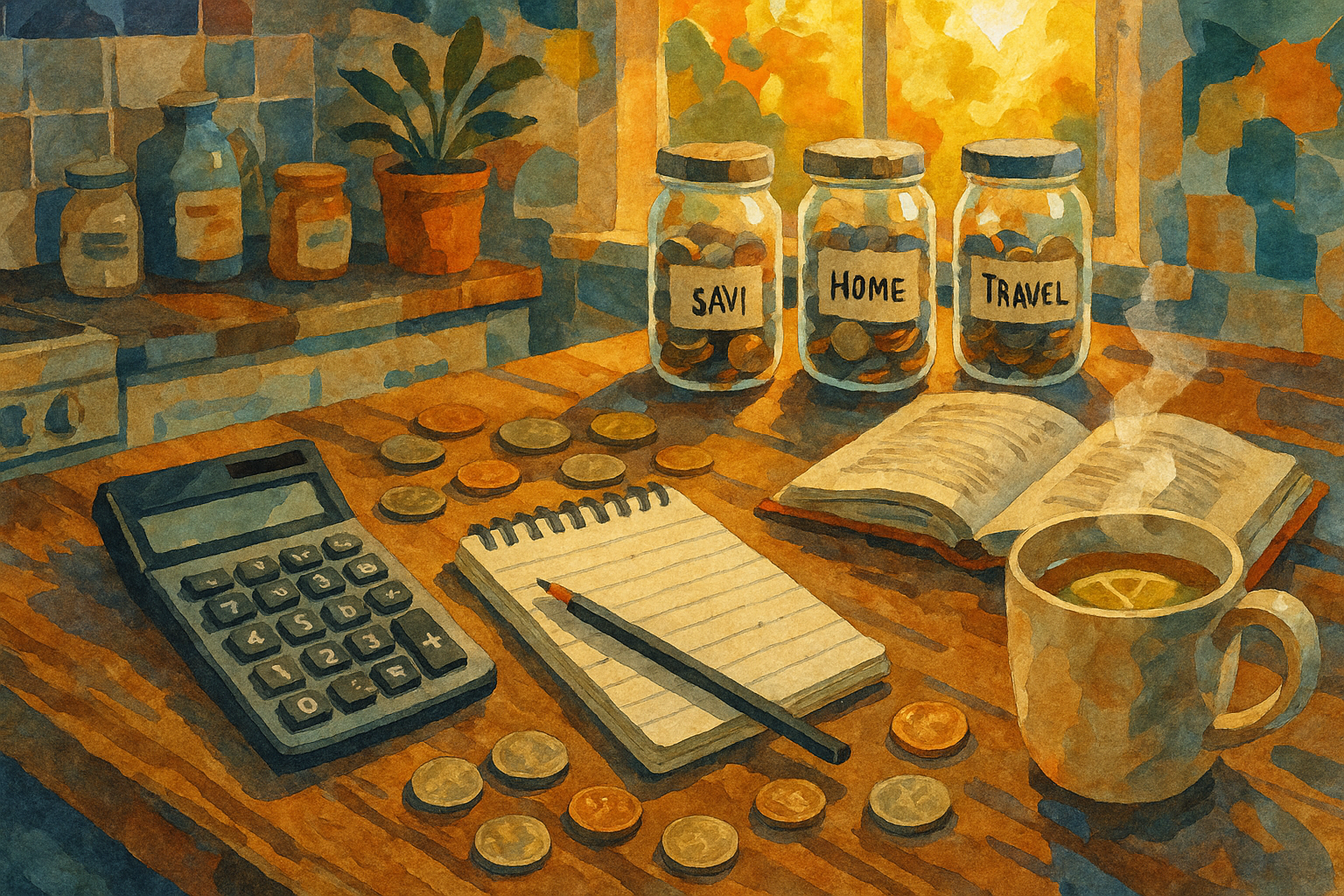

Anyone serious about leaving the 9-to-5 grind needs a concrete target, not vague retirement dreams. The hosts break down the process of calculating your financial independence number using actual expenses—not hypothetical budgets or aspirational spending. The core formula is straightforward: multiply your annual expenses by 25. This gives you the asset base needed to support yourself indefinitely using the 4% withdrawal rule.

The episode emphasizes the critical difference between necessary expenses and lifestyle inflation. By tracking spending patterns, you transform raw data into information that drives decisions. Many high earners wonder why they're barely scraping by despite solid incomes—the answer usually lies in unexamined discretionary spending.

Tax-advantaged accounts like 401ks receive special attention. These tools don't just defer taxes; they fundamentally alter the math of saving by reducing your current taxable income. A dollar contributed pre-tax means you're effectively saving more than a dollar compared to after-tax savings.

The conversation makes clear that financial independence isn't about never spending money again—it's about reclaiming control over your time. The goal is separating your labor from your income, letting investments generate cash flow instead of trading hours for dollars.

Key Topics

Introduction to Financial Independence

Overview of the journey toward financial independence

Understanding Your Why

Knowing your motivations behind pursuing FI

Tracking Expenses

Recognizing necessary versus discretionary spending to optimize finances

Calculating Your FI Number

Deriving your FI number using annual expenses and the 4% rule

The 4% Rule

Guidelines for safe withdrawal rates in retirement

Tax-Advantaged Accounts

How 401k contributions affect your tax situation and savings potential

Next Steps

Implementing these strategies

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Free FI Planning Tools + Community

FI calculator, expense audit, Coast FI tracker, local groups, and 750+ podcast episodes.

No password needed. Free forever.

Action Items

- Track monthly expenses to understand financial habits and identify savings opportunities

- Calculate your FI number by multiplying annual expenses by 25

- Contribute to tax-advantaged accounts like a 401k to enhance savings

Notable Quotes

"Understanding your 'why' leads to knowing your 'how'—that's the essence of FI."

"Transforming data into actionable information is key to effective financial decisions."

"Save not just for retirement, but to reclaim your time."

"Separate working for money and have your investments work for you."

"A common lament, feeling financially stuck despite earning a decent income."

Resources

SmartAsset Tax Calculator: smartasset.com/taxes/income-taxes

Related Episode: How to Get Started - Part 1 (Episode 257)

For more resources, visit choosefi.com/start

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Free FI Planning Tools + Community

FI calculator, expense audit, Coast FI tracker, local groups, and 750+ podcast episodes.

No password needed. Free forever.

Top Travel Card

Ready to unlock a world of free travel? Start with the Chase Sapphire Preferred® Card

$95 annual fee | Earn 100,000 bonus points

Best Card for Side Hustlers and Business Owners

Side hustlers! With the Ink Business Preferred® Credit Card you can earn free travel from your business expenses.

$95 annual fee | Earn 100,000 bonus points

Most Flexible Travel Card

The Capital One Venture Rewards Credit Card can be used to offset almost any travel expense.

$95 annual fee | Earn 75,000 Miles once you spend $4,000 on purchases within 3 months from account opening

ChooseFI has partnered with CardRatings for our coverage of credit card products. ChooseFI and CardRatings may receive a commission from card issuers.