2026 Roth IRA income limits at a glance

Your Modified Adjusted Gross Income (MAGI) determines how much you can contribute directly.

Find your hidden savings in 10 minutes

Our expense audit reveals exactly where your money goes — no budgeting required.

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Free FI Planning Tools + Community

FI calculator, expense audit, Coast FI tracker, local groups, and 750+ podcast episodes.

No password needed. Free forever.

Roth IRA Income Limits for 2026

Knowing the income limit for Roth IRA contributions is the first step to making sure your money ends up where you intend it. The IRS adjusts these thresholds periodically, so it pays to check the current numbers before you contribute each year.

2026 MAGI Thresholds by Filing Status

Data current as of July 2026. Source: IRS Publication 590-A and the IRS COLA announcement for 2026. Verify at IRS.gov before filing.

| Filing Status | Full Contribution (MAGI Below) | Phase-Out Range | No Direct Contribution (MAGI Above) |

|---|---|---|---|

| Single / Head of Household | Under $150,000 | $150,000 – $165,000 | Over $165,000 |

| Married Filing Jointly / Qualifying Surviving Spouse | Under $236,000 | $236,000 – $246,000 | Over $246,000 |

| Married Filing Separately (lived with spouse at any point during the year) | $0 | $0–$10,000 | $10,000 |

Contribution limits for 2026:

- Under age 50: $7,500 per year

- Age 50 and older: $7,500 + $1,100 catch-up per year

Note: The "Married Filing Separately" phase-out range has not been inflation-adjusted in years and remains a narrow $10,000 window regardless of IRS COLA changes.

What Is Modified Adjusted Gross Income (MAGI)?

MAGI is not a line you will find printed on your tax return — it is a calculation. Start with your Adjusted Gross Income (AGI), which appears on Form 1040, Line 11, then add back certain deductions the IRS requires you to include for Roth eligibility purposes.

Common add-backs that can raise your MAGI above your AGI:

- Student loan interest deduction

- Foreign earned income exclusion

- Tuition and fees deduction (when applicable)

- Deductible IRA contributions (if you took them)

- Rental losses from passive activity

Why does this matter? Many people assume their W-2 income is their MAGI. For straightforward employees with no investment income or deductions, that is often close — but not always identical. If you have a side business, rental property, or foreign income, your MAGI can be meaningfully higher than your W-2 wages.

Practical tip: To calculate your Roth MAGI precisely, work through Worksheet 2-1 in IRS Publication 590-A. This is the IRS's own tool for this calculation and takes about 10 minutes if you have your return in front of you.

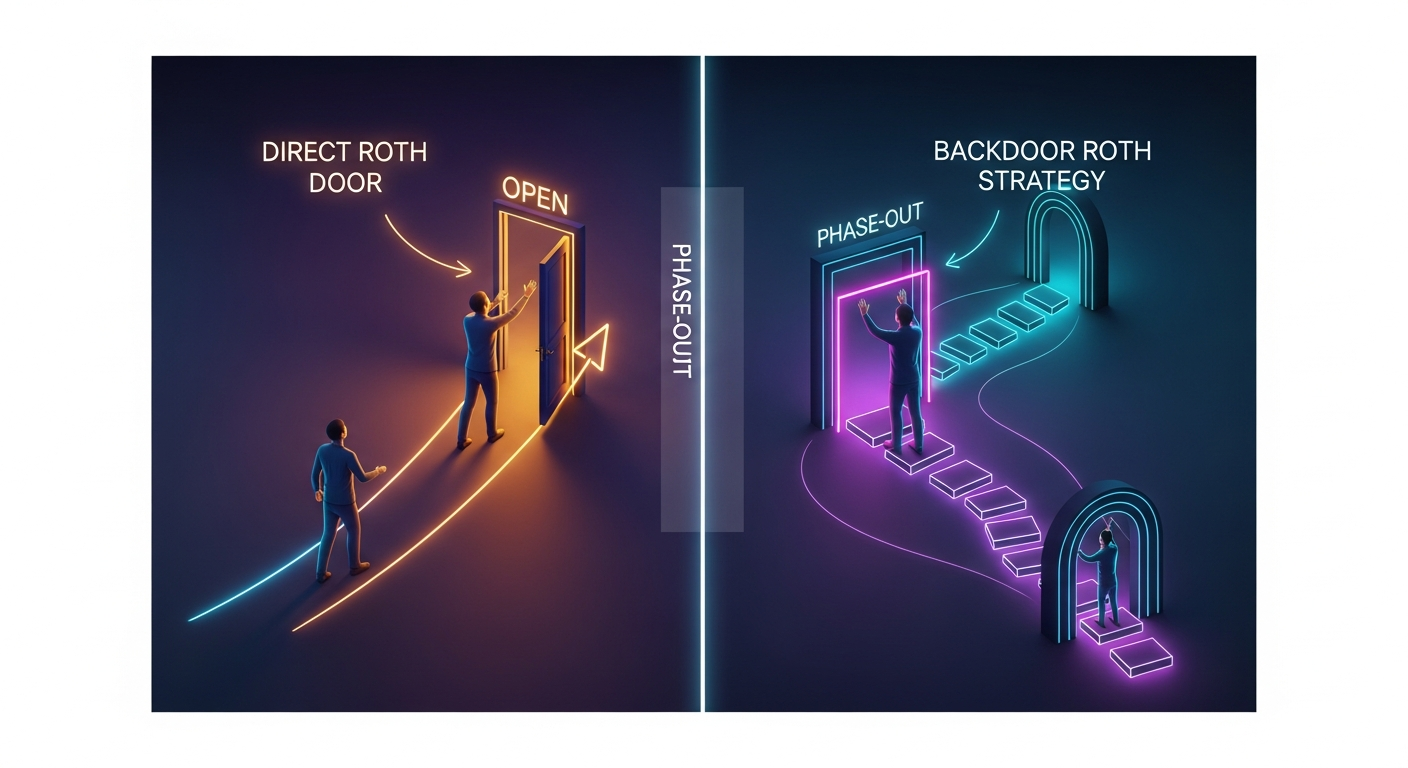

The Phase-Out Range: Partial Contributions

If your MAGI falls inside the phase-out range, you are not locked out entirely — but your maximum allowable contribution shrinks proportionally as your income rises through the range.

The formula:

Round the result down to the nearest $10. If the calculation produces a number between $1 and $199, the IRS allows a minimum contribution of $200.

Worked example (Single filer):

Suppose you are a single filer with a MAGI of $158,000 in 2026. Using the 2026 single filer phase-out range (verify exact figures at IRS.gov):

- Subtract your MAGI from the upper phase-out limit

- Divide by the total width of the phase-out range

- Multiply by the full contribution limit ($7,000 if under 50)

- Round down to the nearest $10

The result is your reduced contribution maximum for the year. Run this calculation after your income is finalized — not mid-year estimates — to avoid excess contribution penalties.

If you are in the phase-out range, consider the backdoor Roth IRA instead. Rather than making a partial direct contribution, you contribute to a traditional IRA (no income limit on contributions) and then convert it to a Roth. You get the full $7,000 (or $8,000) in, and you avoid tracking a partial contribution limit each year. It involves one extra step but is generally cleaner — especially if you expect to stay in or above the phase-out range for multiple years.

One caution: The backdoor Roth works cleanly only if you have no pre-tax money sitting in other traditional, SEP, or SIMPLE IRA accounts. If you do, the pro-rata rule applies and can create an unexpected tax bill. Check with a tax professional if this applies to your situation.

What Happens If You Exceed the Roth IRA Income Limit

Contributing to a Roth IRA when your income is too high isn't just a paperwork issue — the IRS has a specific penalty mechanism that compounds over time if left uncorrected.

Excess Contributions and the 6% Penalty

If you contribute to a Roth IRA in a year when your MAGI exceeds the income limit for Roth IRA eligibility, the IRS classifies the contribution as an excess contribution. The penalty is a 6% excise tax on the excess amount, and it's assessed every year the excess remains in your account.

That means if you contributed $7,000 when you weren't eligible and do nothing, you owe 6% this year — and 6% again next year, and the year after that. The longer it sits uncorrected, the more you pay. This isn't a one-time slap on the wrist; it's an annual charge until you fix it.

How to Fix an Excess Contribution

There are three legitimate ways to correct an excess contribution:

Option 1: Withdraw the excess plus earnings before your tax filing deadline (including extensions). The IRS allows you to pull out the excess contribution and any earnings it generated. The earnings portion will be taxable as ordinary income, and if you're under 59½, it may also be subject to the 10% early withdrawal penalty.

Option 2: Recharacterize the contribution as a Traditional IRA contribution. If you're eligible to contribute to a Traditional IRA, you can recharacterize your Roth contribution before the tax filing deadline. This effectively relabels the contribution — your money stays invested, just in a different account type.

Option 3: Apply the excess to the following year's contribution. If you expect your MAGI to fall below the income limit for Roth IRA contributions next year, you can carry the excess forward and apply it to next year's limit. This only works if you'll actually be eligible in the following year.

Practical tip: The cleanest way to sidestep this situation entirely is the backdoor Roth IRA — contribute to a Traditional IRA first, then convert it to a Roth. No income-based eligibility check required.

Prevention Is Better Than Correction

If your income is near the phase-out range or genuinely unpredictable — due to a year-end bonus, equity compensation, or freelance income — guessing whether you're under the income limit for a Roth IRA adds unnecessary risk. The backdoor Roth IRA eliminates that guesswork entirely.

You don't need to estimate your MAGI each year or scramble to correct mistakes after the fact. Use the backdoor path every year regardless of your income level, and the question of whether you exceeded the limit simply never comes up.

The Backdoor Roth IRA: Step-by-Step

A two-step strategy that lets high earners contribute to a Roth IRA regardless of income

What Is the Backdoor Roth IRA?

The Backdoor Roth IRA is not a special account — it is a two-step strategy that works around the income limit for Roth IRA contributions. Step one: contribute to a Traditional IRA (there is no income limit for non-deductible contributions). Step two: convert that Traditional IRA balance to a Roth IRA. The IRS officially acknowledges this approach, and it is widely used by high earners and FI community members who are phased out of direct Roth contributions. Congress has considered closing this strategy multiple times but has not done so as of 2026.

Step 1 — Check for Existing Pre-Tax IRA Balances

Before anything else, confirm whether you have any pre-tax money sitting in a Traditional IRA, SEP IRA, or SIMPLE IRA. If you do, the pro rata rule applies and could make your conversion partially taxable. Resolve this first — details in the pro rata section below.

Step 2 — Open a Traditional IRA

If you do not already have a Traditional IRA, open one at a brokerage you trust. Fidelity, Vanguard, and Schwab all support the backdoor conversion process and have clear instructions for completing it online.

Step 3 — Make a Non-Deductible Contribution

Contribute the maximum allowed amount for 2026: $7,000 if you are under age 50, or $8,000 if you are 50 or older. Do not deduct this contribution on your taxes — it is a non-deductible contribution, which is what makes the eventual conversion tax-free.

Step 4 — Wait for the Contribution to Settle

Some brokerages allow you to convert immediately; others require 1–3 business days for the funds to settle before you can proceed. Check your brokerage's specific process. Leaving the money sitting in a money market fund during this window keeps earnings near zero, which simplifies your tax math.

Step 5 — Convert to Your Roth IRA

Once settled, convert the entire Traditional IRA balance to your Roth IRA. This is technically a taxable event — but if the contribution was non-deductible and no earnings have accumulated, the tax owed is $0 or negligible. The converted funds then grow tax-free inside your Roth. Many FI community members do this in January each year so the full amount compounds tax-free for the rest of the year.

Step 6 — File IRS Form 8606

When you file your tax return, include IRS Form 8606. This form reports your non-deductible contribution and documents the conversion. Filing it correctly each year creates a paper trail that protects you from being taxed again on those dollars when you withdraw in retirement. Do not skip this step.

The Pro Rata Rule — The Most Important Thing to Understand

If you have ANY pre-tax money in a Traditional IRA, SEP IRA, or SIMPLE IRA, the IRS applies the pro rata rule to your conversion. The taxable portion of your conversion is proportional to the ratio of pre-tax dollars across all your Traditional IRAs. Example: you have $93,000 in pre-tax Traditional IRA funds and contribute $7,000 non-deductible. Your total Traditional IRA balance is $100,000. Only 7% of your conversion is tax-free — the other 93% is taxable income, which defeats the purpose entirely. The fix: roll all pre-tax Traditional IRA funds into your employer 401(k) plan (if it accepts incoming rollovers) before doing the backdoor conversion. This zeros out your pre-tax Traditional IRA balance, making the conversion tax-free. For holding period rules on converted funds, see the [Roth IRA 5-Year Rule Explained](/roth-ira-5-year-rule). For the broader Roth vs. Traditional analysis above the income limit for Roth IRA, see [Roth vs. Traditional IRA Over the Income Limit](/roth-vs-traditional-ira-income-limits).

What Is the Backdoor Roth IRA?

The Backdoor Roth IRA is not a special account — it is a two-step strategy that works around the income limit for Roth IRA contributions. Step one: contribute to a Traditional IRA (there is no income limit for non-deductible contributions). Step two: convert that Traditional IRA balance to a Roth IRA. The IRS officially acknowledges this approach, and it is widely used by high earners and FI community members who are phased out of direct Roth contributions. Congress has considered closing this strategy multiple times but has not done so as of 2026.

Step 1 — Check for Existing Pre-Tax IRA Balances

Before anything else, confirm whether you have any pre-tax money sitting in a Traditional IRA, SEP IRA, or SIMPLE IRA. If you do, the pro rata rule applies and could make your conversion partially taxable. Resolve this first — details in the pro rata section below.

Step 2 — Open a Traditional IRA

If you do not already have a Traditional IRA, open one at a brokerage you trust. Fidelity, Vanguard, and Schwab all support the backdoor conversion process and have clear instructions for completing it online.

Step 3 — Make a Non-Deductible Contribution

Contribute the maximum allowed amount for 2026: $7,000 if you are under age 50, or $8,000 if you are 50 or older. Do not deduct this contribution on your taxes — it is a non-deductible contribution, which is what makes the eventual conversion tax-free.

Step 4 — Wait for the Contribution to Settle

Some brokerages allow you to convert immediately; others require 1–3 business days for the funds to settle before you can proceed. Check your brokerage's specific process. Leaving the money sitting in a money market fund during this window keeps earnings near zero, which simplifies your tax math.

Step 5 — Convert to Your Roth IRA

Once settled, convert the entire Traditional IRA balance to your Roth IRA. This is technically a taxable event — but if the contribution was non-deductible and no earnings have accumulated, the tax owed is $0 or negligible. The converted funds then grow tax-free inside your Roth. Many FI community members do this in January each year so the full amount compounds tax-free for the rest of the year.

Step 6 — File IRS Form 8606

When you file your tax return, include IRS Form 8606. This form reports your non-deductible contribution and documents the conversion. Filing it correctly each year creates a paper trail that protects you from being taxed again on those dollars when you withdraw in retirement. Do not skip this step.

The Pro Rata Rule — The Most Important Thing to Understand

If you have ANY pre-tax money in a Traditional IRA, SEP IRA, or SIMPLE IRA, the IRS applies the pro rata rule to your conversion. The taxable portion of your conversion is proportional to the ratio of pre-tax dollars across all your Traditional IRAs. Example: you have $93,000 in pre-tax Traditional IRA funds and contribute $7,000 non-deductible. Your total Traditional IRA balance is $100,000. Only 7% of your conversion is tax-free — the other 93% is taxable income, which defeats the purpose entirely. The fix: roll all pre-tax Traditional IRA funds into your employer 401(k) plan (if it accepts incoming rollovers) before doing the backdoor conversion. This zeros out your pre-tax Traditional IRA balance, making the conversion tax-free. For holding period rules on converted funds, see the [Roth IRA 5-Year Rule Explained](/roth-ira-5-year-rule). For the broader Roth vs. Traditional analysis above the income limit for Roth IRA, see [Roth vs. Traditional IRA Over the Income Limit](/roth-vs-traditional-ira-income-limits).

The Mega Backdoor Roth: The Advanced Play

If you've already hit the standard income limit for Roth IRA contributions and you're looking for more ways to build tax-free wealth, the mega backdoor Roth is worth understanding. It's a more complex strategy, but for high earners pursuing FI, the numbers can be significant.

What Is the Mega Backdoor Roth?

The mega backdoor Roth is a strategy that lets you make after-tax contributions to your employer's 401(k) plan — separate from your standard pre-tax or Roth 401(k) contributions — and then convert those funds into a Roth IRA or Roth 401(k).

Here's how the math works: The IRS sets a total annual additions limit for 401(k) plans that covers all contributions — employee contributions, employer match, and after-tax contributions combined. The gap between that total limit and what you and your employer have already contributed is your available after-tax contribution space.

Example: If the total limit is $70,000 and you contribute $23,500 pre-tax while your employer adds a $10,000 match, you have up to $36,500 in after-tax contribution space available for a mega backdoor Roth conversion.

Once those after-tax dollars are in the plan, you convert them to Roth — either inside the plan or by rolling them out to a Roth IRA. The result: tax-free growth on a much larger pool of money than the standard Roth IRA contribution limit allows.

Requirements — Does Your Plan Allow It?

Not every 401(k) plan supports this strategy. To use the mega backdoor Roth, your plan must allow both of the following:

- After-tax (non-Roth) contributions to the 401(k)

- In-plan Roth conversions OR in-service withdrawals/rollovers to an external Roth IRA

If your plan only allows after-tax contributions but not the conversion or rollout step, the strategy doesn't work as intended — earnings on after-tax contributions are taxable, so you want to convert quickly.

How to check: Contact your plan administrator directly or pull up your Summary Plan Description (SPD). Ask specifically: "Does our plan allow after-tax contributions and in-plan Roth conversions or in-service distributions?"

The good news is that more employers are adding this feature as awareness grows. If your current plan doesn't support it, it's worth raising with your HR or benefits team — especially at larger companies where plan redesigns happen regularly.

Why This Matters for FI

The standard income limit for Roth IRA contributions phases out for high earners, and even when you can contribute (or use the backdoor Roth IRA), the annual limit of $7,000–$8,000 feels small relative to aggressive FI savings targets.

The mega backdoor Roth changes that math entirely. Depending on your employer match and plan structure, you could move $30,000–$46,000+ per year into Roth accounts through this strategy alone — on top of your standard Roth IRA contribution.

For a married couple both using this approach and both contributing to backdoor Roth IRAs, it's realistic to move $80,000–$100,000+ into Roth accounts in a single year. Over a 10–15 year FI timeline, that's a substantial tax-free base that won't be subject to required minimum distributions and can be accessed flexibly in early retirement.

For high earners who expect to be in a lower tax bracket after reaching FI, front-loading Roth conversions now can mean significantly less tax drag later.

- Want to think through whether Roth or Traditional contributions make more sense inside your 401(k)? See Roth 401(k) vs Traditional in Peak Income Years.

- For the full picture on advanced tax strategies, including Roth conversions and beyond, see Roth IRA Conversion and Other Advanced Tax Strategies.

Why the Roth IRA Is the Most Important Account for Early Retirees

If you're pursuing FI and planning to retire well before age 65, the Roth IRA is the single most powerful account in your toolkit. Unlike a traditional 401(k) or IRA, the Roth is built in a way that rewards exactly the behaviors early retirees rely on: low taxable income, flexible withdrawals, and decades of tax-free compounding. Here's why it earns its place at the center of any FI withdrawal plan.

Tax-Free Growth, Tax-Free Withdrawals

Contributions to a Roth IRA grow tax-free, and qualified withdrawals — after age 59½ and the 5-year rule — come out completely tax-free. For early retirees, that matters in ways that go beyond simple tax savings.

When you have no employer income, you control your taxable income. Keep it low enough and you may qualify for ACA premium tax credits, the 0% long-term capital gains bracket, or other income-dependent benefits. Tax-free Roth withdrawals don't count as income for those calculations — giving you real flexibility to manage your tax picture year by year.

No Required Minimum Distributions

Traditional IRAs and 401(k)s force you to start taking distributions at age 73 under SECURE 2.0 rules, whether you need the money or not. Those mandatory withdrawals can push you into higher tax brackets, trigger Medicare surcharges, and complicate income-based benefit calculations.

Roth IRAs have no required minimum distributions during the owner's lifetime. Your money can keep growing tax-free for as long as you live. That also makes the Roth an effective inheritance vehicle — heirs receive tax-free assets rather than a deferred tax bill.

Contributions Are Accessible Penalty-Free at Any Age

One of the most misunderstood features of the Roth IRA is contribution access. You can withdraw the money you've contributed — not earnings, just contributions — at any time, at any age, for any reason, with no tax and no penalty.

This turns your Roth into a built-in bridge for early retirement. If you retire before 59½ and need flexibility before other accounts are accessible, your contribution dollars are already available. It's not a loophole; it's how the account is designed.

The Roth Conversion Ladder — The FI Withdrawal Strategy

For most people in the FI community, the Roth conversion ladder is the core strategy for funding early retirement. Here's how it works: each year in early retirement, you convert a portion of your traditional IRA or 401(k) funds into a Roth IRA. Because your earned income is low or zero, you pay taxes on those conversions at a low marginal rate. After five years, each converted amount becomes accessible penalty-free.

Done consistently, this creates a rolling pipeline of accessible, tax-advantaged funds — one layer of conversions becoming available each year like clockwork. It takes planning and a multi-year runway before retirement, but the payoff is significant.

For the full mechanics, see the complete ladder strategy and Roth conversion optimization tactics.

The Roth Is a Multi-Generational FI Tool

The Roth IRA's advantages don't stop with you. Any child or teenager with earned income — from a part-time job, lawn mowing, or babysitting — can open a Roth IRA. Contributions made at age 15 have four or five decades of tax-free compounding ahead of them.

Note that the same income limit for Roth IRA eligibility that applies to adults also applies to kids: contributions can't exceed the child's earned income for the year, and the standard annual contribution limits apply.

Learn more about when and why your child should open a Roth IRA, how to open a Roth IRA for kids, and how to use a Roth IRA for college and other expenses — including the flexibility the account offers beyond retirement.

For the full tax-advantaged playbook, see what to do after maxing your retirement accounts.

2026 Roth IRA income phase-out ranges

| Filing Status | Full Contribution | Phase-Out Range | No Direct Contribution |

|---|---|---|---|

| Single / Head of Household | Under $150,000 | $150,000 – $165,000 | Over $165,000 |

| Married Filing Jointly | Under $236,000 | $236,000 – $246,000 | Over $246,000 |

| Married Filing Separately | N/A | $0–$10,000 | Over $10,000 |

MAGI = Modified Adjusted Gross Income. Phase-out means your contribution limit is reduced proportionally. Use the backdoor Roth strategy if above these limits.

Execute the backdoor Roth IRA strategy

If your income exceeds the limit, here's how to contribute anyway.

Confirm your traditional IRA balance is $0

The backdoor Roth works cleanly only if you have no pre-tax traditional IRA money. If you do, you'll trigger the pro-rata rule and owe taxes on a portion of the conversion. Roll any existing traditional IRA into your 401(k) first.

Pro tip: The pro-rata rule looks at ALL your traditional IRA accounts combined, including SEP and SIMPLE IRAs.

Contribute to a traditional IRA (non-deductible)

Open a traditional IRA (or use your existing one) and contribute the max: $7,000 if under 50, $8,000 if 50+. This contribution is non-deductible — you won't claim a tax deduction.

Convert to Roth IRA immediately

Call your brokerage or click "Convert to Roth" in your account. Since you contributed after-tax dollars and had $0 in pre-tax IRA money, the conversion is tax-free. Don't wait — convert the same day or next business day.

File Form 8606 with your taxes

Report the non-deductible contribution on IRS Form 8606. Your tax software (TurboTax, H&R Block) will handle this automatically if you enter the contribution and conversion correctly.

Frequently Asked Questions

Your eligibility depends on your Modified Adjusted Gross Income (MAGI) and filing status. For single filers, the phase-out range begins at $150,000 and ends at $165,000 — above that, direct contributions are not allowed. For married filing jointly, the phase-out runs from $236,000 to $246,000. Married filing separately faces a much stricter threshold: the phase-out starts at $0 and ends at $10,000, effectively eliminating direct contributions for most people in that category. See the full income limit table earlier in this post for a complete breakdown by filing status.

It depends on your filing status. Single filers earning between $150,000 and $165,000 fall in the phase-out range and may still make a partial contribution — the allowed amount decreases gradually as income rises. Above $165,000, direct contributions are not permitted for single filers. However, regardless of income or filing status, the backdoor Roth IRA is available to everyone. This strategy lets high earners contribute to a Traditional IRA and convert it to a Roth, with no income ceiling on the conversion itself.

The backdoor Roth IRA is a two-step process: you make a non-deductible contribution to a Traditional IRA, then convert that balance to a Roth IRA shortly after. It is a fully legal strategy — acknowledged by the IRS and widely used by high-income earners who exceed the direct contribution income limits. For a step-by-step walkthrough of exactly how to execute this, see the backdoor Roth section earlier in this post.

The pro rata rule determines how much of a Roth conversion is taxable when you hold both pre-tax and after-tax funds across all your Traditional IRAs. If you have existing pre-tax IRA money, the IRS treats your conversion as a proportional mix of taxable and non-taxable funds — not just the after-tax portion you intended to convert. This can create an unexpected tax bill. The most effective fix: roll your pre-tax Traditional IRA funds into an employer 401(k) before doing the backdoor Roth, leaving only after-tax basis in your IRA.

An excess contribution triggers a 6% excise tax penalty on the amount over the limit, and that penalty applies every year the excess remains in the account uncorrected. You have three ways to fix it: withdraw the excess contribution plus any earnings before the tax filing deadline (including extensions), recharacterize the contribution to a Traditional IRA, or leave it and apply it as a contribution toward the next tax year if you are eligible then. Acting quickly limits the penalty — the longer the excess sits, the more tax years it affects.

The mega backdoor Roth allows you to contribute after-tax dollars to a 401(k) — beyond the standard pre-tax or Roth 401(k) limits — and then convert those funds to Roth. Depending on your plan, this can add $30,000 to $46,000 or more per year in Roth-eligible contributions on top of standard limits. There is a catch: your employer's 401(k) plan must specifically allow after-tax contributions and either in-plan Roth conversions or in-service withdrawals. Not all plans support this, so check your Summary Plan Description or contact your plan administrator.

Yes. There is no income limit on making non-deductible Traditional IRA contributions, and there is no limit on how many times you can convert to a Roth. Many people in the FI community treat this as an annual January task — contribute to a Traditional IRA for the new year, convert immediately, and move on. As long as you track your non-deductible contributions using IRS Form 8606, you will not be double-taxed on the amount you already paid tax on.

The Roth IRA is one of the most flexible accounts available for early retirees. Qualified withdrawals are completely tax-free, and unlike Traditional IRAs or 401(k)s, Roth IRAs have no Required Minimum Distributions (RMDs) during your lifetime. You can also withdraw your contributions (not earnings) at any time, penalty-free — a feature that makes Roth accounts useful even before age 59½. For those retiring early, the Roth conversion ladder is a key strategy for accessing tax-advantaged funds without penalties. To go deeper, read Why You Should Fund Your Roth Even If You Won't Need It and the full account hierarchy guide on Tax-Advantaged Investing.

The Income Limit Is a Decision Tree, Not a Dead End

Every income level has a clear path into a Roth account — here is how to find yours

If your modified adjusted gross income falls below the phase-out range, you can contribute directly to a Roth IRA up to the annual limit. This is the most straightforward path: open an account, fund it, and let tax-free growth do the work for decades.

If your income sits inside the phase-out window, a partial direct contribution gets messy fast. The backdoor Roth IRA is actually cleaner: contribute to a traditional IRA, then convert immediately. No guessing, no partial calculations, no income limit problem.

High earners have two routes running in parallel. The backdoor Roth IRA handles your personal contribution. The mega backdoor Roth — funded through after-tax 401(k) contributions converted in-plan — can add tens of thousands more in Roth dollars annually. Check whether your 401(k) plan allows after-tax contributions and in-service conversions.

For FI seekers planning to retire before 59½, the Roth conversion ladder is the withdrawal engine that makes it work. Convert traditional IRA or 401(k) funds to Roth each year in early retirement, wait five years per conversion, and pull funds tax-free and penalty-free. No required minimum distributions, no forced taxable income in later years — just flexibility.

The income limit for Roth IRA contributions is not a reason to skip the Roth — it is a signal to use the right strategy for your income level. Tax-free growth, tax-free withdrawals, and no RMDs make the Roth non-negotiable as a foundation for early retirement. Read the full framework in the ChooseFI Tax Strategy and Planning Guide at /tax-strategies, then use the FI calculator to model exactly how Roth contributions accelerate your timeline. Connect with others working through the same decisions inside the ChooseFI community — and sign up for the newsletter to get tax strategy breakdowns delivered directly to you.

If your modified adjusted gross income falls below the phase-out range, you can contribute directly to a Roth IRA up to the annual limit. This is the most straightforward path: open an account, fund it, and let tax-free growth do the work for decades.

If your income sits inside the phase-out window, a partial direct contribution gets messy fast. The backdoor Roth IRA is actually cleaner: contribute to a traditional IRA, then convert immediately. No guessing, no partial calculations, no income limit problem.

High earners have two routes running in parallel. The backdoor Roth IRA handles your personal contribution. The mega backdoor Roth — funded through after-tax 401(k) contributions converted in-plan — can add tens of thousands more in Roth dollars annually. Check whether your 401(k) plan allows after-tax contributions and in-service conversions.

For FI seekers planning to retire before 59½, the Roth conversion ladder is the withdrawal engine that makes it work. Convert traditional IRA or 401(k) funds to Roth each year in early retirement, wait five years per conversion, and pull funds tax-free and penalty-free. No required minimum distributions, no forced taxable income in later years — just flexibility.

The income limit for Roth IRA contributions is not a reason to skip the Roth — it is a signal to use the right strategy for your income level. Tax-free growth, tax-free withdrawals, and no RMDs make the Roth non-negotiable as a foundation for early retirement. Read the full framework in the ChooseFI Tax Strategy and Planning Guide at /tax-strategies, then use the FI calculator to model exactly how Roth contributions accelerate your timeline. Connect with others working through the same decisions inside the ChooseFI community — and sign up for the newsletter to get tax strategy breakdowns delivered directly to you.

The Bottom Line

Roth IRA income limits exist, but they don't actually prevent high earners from contributing. The backdoor Roth IRA is a straightforward, IRS-acknowledged strategy that takes 15 minutes once a year. For FI-focused investors, the Roth IRA is the most valuable account in your stack — tax-free growth, no RMDs, and penalty-free access to contributions at any age. Max it out every year, regardless of your income.

2026 contribution limit

$7,000

Single income phase-out starts

$150K

MFJ income phase-out starts

$236K

Find Your Hidden Savings in 10 Minutes

Free tools to audit your spending, model your FI timeline, and optimize every dollar.

Explore Tools