Roth IRA 5-Year Rule Explained (2026 Guide)

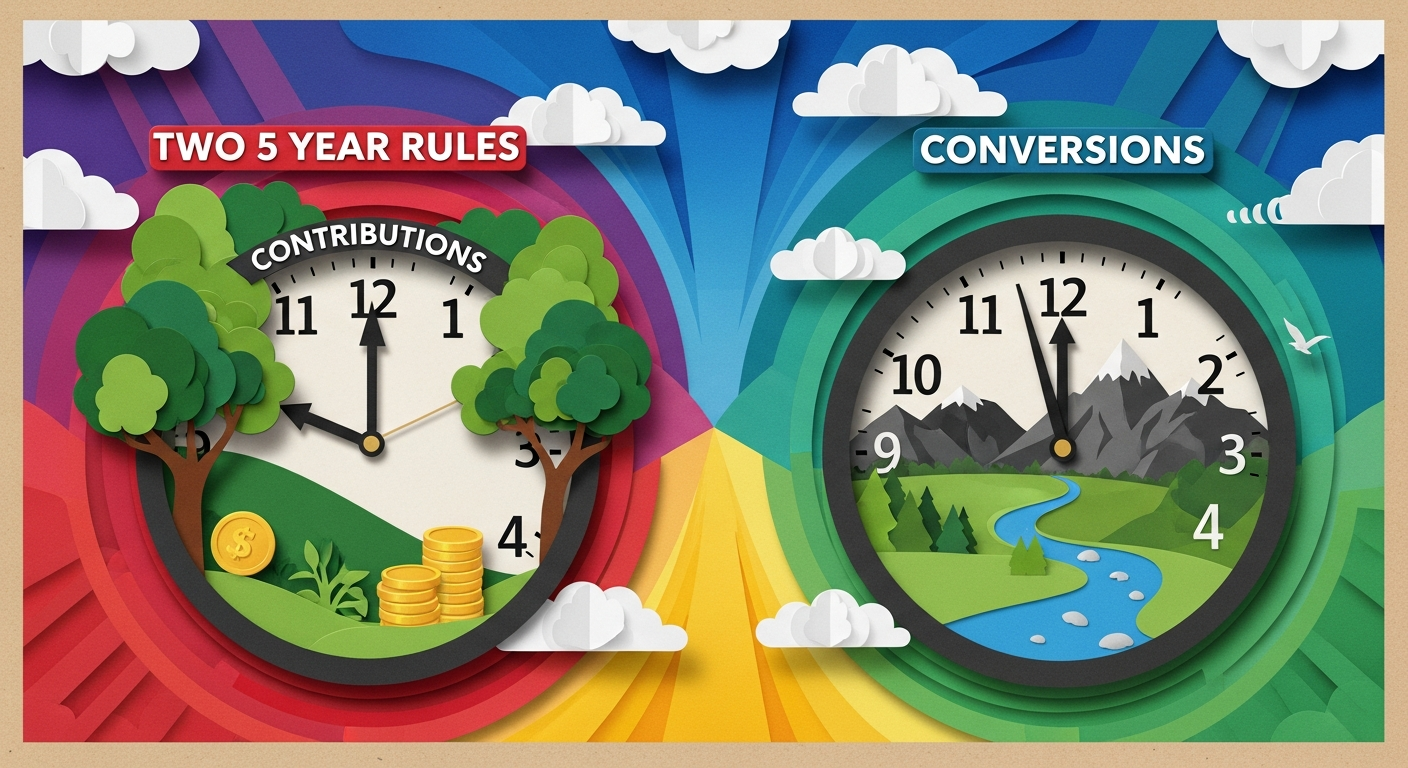

There are actually two separate Roth IRA 5-year rules. One governs tax-free earnings withdrawals, the other affects early withdrawal penalties on conv...

Read articleSmart tax planning is the secret weapon of financial independence. Learn strategies that can save you thousands every year.

Six powerful strategies to minimize your tax burden and accelerate your path to FI.

Convert traditional IRA/401k to Roth during low-income years. After 5 years, withdraw contributions tax-free. Perfect for early retirees.

Contribute pre-tax, grow tax-free, withdraw tax-free for medical expenses. The only account with triple tax benefits.

Sell investments at a loss to offset capital gains. Harvest up to $3,000 against ordinary income annually.

Maximize employer matches and contribution limits. Traditional vs. Roth depends on your current vs. future tax bracket.

Hold investments 12+ months for long-term rates. In the 0% bracket? Harvest gains for free basis step-up.

Some states have no income tax. Relocating in early retirement can save significant money over decades.

Understand how marginal tax brackets work and see where your income falls.

2026 federal income tax brackets. For educational purposes only — consult a tax professional for personalized advice.

Different strategies apply at different stages of your financial independence path.

Key focus: Reduce taxable income now while building your investment base for the future.

Key focus: The years between leaving work and Social Security are your golden conversion window.

Key focus: Minimize lifetime taxes with strategic withdrawals and proactive Roth conversions.

In-depth guides on tax optimization, Roth conversions, and FI-specific tax planning.

There are actually two separate Roth IRA 5-year rules. One governs tax-free earnings withdrawals, the other affects early withdrawal penalties on conv...

Read articleCalculate how much you need — takes 60 seconds.

Your FI number in 60 seconds

Simple inputs, instant results

See your freedom date

Based on your savings rate and goals

Track your progress

Free tools used by thousands of members