What's your FI number? Calculate it in 60 seconds

The one number that changes everything

The 4% Rule in Numbers

Model your path to retirement

Test withdrawal strategies and see how long your portfolio lasts.

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Join 25,000+ on the Path to FI

Free access to FI tools, forums, local groups, and 750+ episodes.

No password needed. Free forever.

Imagine this: You're planning for a future where work becomes optional — not at 65, but maybe in your 30s or 40s. That’s decades of freedom ahead… but also decades of financial responsibility. The classic 4% rule was designed with a 30-year retirement in mind. But what happens when your retirement might stretch 40, even 50 years?

That’s exactly what Rachel is wondering:

FI Number by Annual Spending

Your FI number = Annual expenses × 25

| Annual Expenses | FI Number (4%) | FI Number (3.5%) | Monthly Withdrawal |

|---|---|---|---|

Based on the 4% rule (×25) and a more conservative 3.5% rate (×28.6).

Hi! I have a question related to the 4% rule. It typically comes with the caveat that funds will last 30 years. What about those of us looking to RE in our 30s and 40s? What rule should we be using for 50+ years?

Listen to the Answer

Apply the 4% Rule to Your Retirement Plan

Calculate your FI number and determine when you can retire.

Calculate your annual expenses

1 hourTrack every dollar you spend for at least 3 months, then annualize. Include housing, food, transportation, insurance, healthcare, and discretionary spending. This is the foundation of your FI number.

Pro tip: Use your actual spending, not a budget — most people underestimate by 10-20%.

Multiply by 25 for your FI number

5 minutesYour annual expenses × 25 = your FI number using the standard 4% rule. For example, if you spend $40,000/year, your FI number is $1,000,000.

Pro tip: For early retirement (40+ years), consider using 28-30× for a more conservative target.

Build a flexible withdrawal strategy

30 minutesPlan to withdraw 4% in year one, then adjust for inflation. In bad market years, consider reducing withdrawals slightly; in good years, you can spend a bit more. Flexibility dramatically improves success rates.

Pro tip: Variable percentage withdrawal (VPW) or guardrails strategies can improve on the rigid 4% rule.

Understanding the 4% Rule

Origins and Assumptions

The 4% rule, introduced by financial planner Bill Bengen in the 1990s, revolutionized retirement planning. The rule was born out of a simple yet crucial question: How much can one safely withdraw from their retirement savings annually, without the risk of running out of money? The Trinity Study later validated Bengen's approach, confirming that a 4% initial withdrawal rate, adjusted annually for inflation, would likely allow retirees to maintain their nest egg for at least 30 years in most historical scenarios.

Several key assumptions underpin the 4% rule:

- 30-Year Retirement Period: The rule was specifically designed for a retirement span of 30 years.

- Acceptance of Asset Depletion: The rule considers a scenario where, at the end of 30 years, your portfolio might be significantly depleted. As long as your funds last through your retirement, it's considered a success, even if there's little left for inheritance.

Common Misunderstandings

Within the Financial Independence, Retire Early (FIRE) community, there's a tendency to overlook some of the foundational assumptions of the 4% rule. Many assume that the rule guarantees perpetual preservation of purchasing power, but in truth, it's built on the premise of asset depletion. The notion that your portfolio might not maintain its purchasing power can be unsettling, especially if you're contemplating a retirement that could extend well beyond 30 years.

The Challenge of Longer Horizons

The Two Camps

When it comes to planning for an extended retirement horizon, people often fall into two camps:

- Overly Cautious: This group believes that if your retirement is going to be twice as long, you need to save twice as much money. It’s a daunting prospect, suggesting that one must accumulate a colossal nest egg to ensure financial security.

- Overly Optimistic: The other camp is hopeful, sometimes overly so. They point to average or median retirement outcomes that show substantial nest eggs even after 30 years and assume this trend will continue indefinitely.

Both perspectives miss a crucial point: the time value of money. You don't need to set aside as much for later retirement years as you do for the early years, thanks to the principle that money invested today can grow over time. But you should set aside at least some extra funds to account for the longer horizon.

The Middle Ground

Finding the middle ground involves understanding the importance of financial principles like the time value of money and running historical simulations to determine safe withdrawal rates. This approach provides a more nuanced view of what is required for a sustainable retirement plan that spans 50 years or more.

Safe Withdrawal Rates for Extended Horizons

Historical Data and Simulations

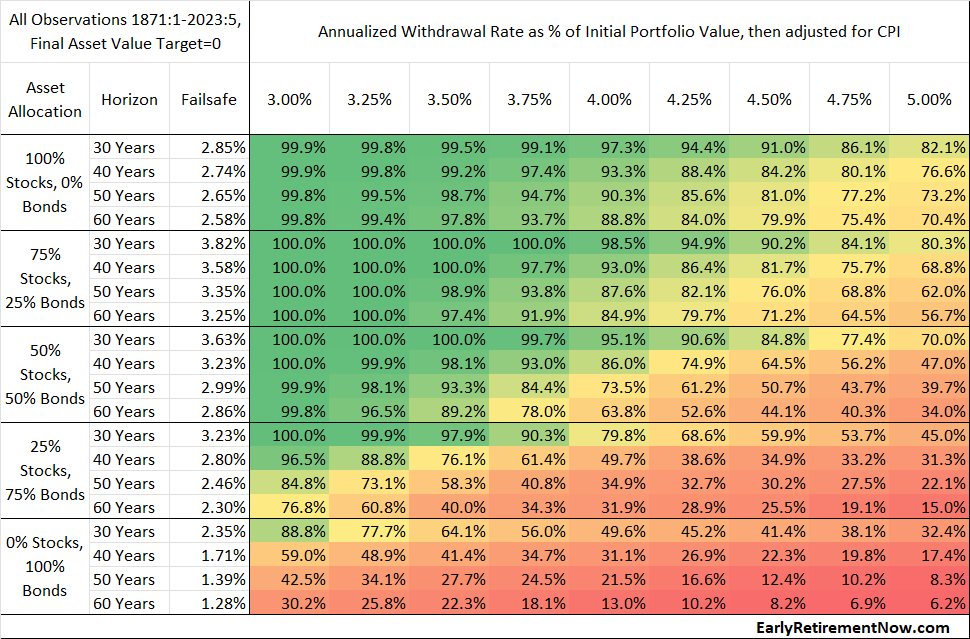

To address the needs of those looking to retire early, it's essential to consider historical data and simulations that extend beyond the typical 30-year horizon. Here are some key findings from my research:

Safe Withdrawal Rates for Different Horizons

| Retirement Horizon | Fail-Safe Withdrawal Rate |

|---|---|

| 30 Years | 3.82% |

| 40 Years | 3.58% |

| 50 Years | 3.35% |

| 60 Years | 3.25% |

These figures reflect a decline in safe withdrawal rates as the retirement horizon extends, but they offer much-needed clarity and guidance.

Practical Implications

Understanding these rates can have significant implications for your retirement budget. For example:

- With a $1 million portfolio, a 30-year retirement allows for an annual budget of $38,200. However, for a 50-year retirement, you would adjust to $32,500 annually to ensure longevity.

- If your goal is a $50,000 annual retirement budget, you’d need approximately $1.3 million for a 30-year horizon and about $1.5 million for a 60-year horizon.

The Good News for Early Retirees

Realistic Adjustments

The good news? Doubling your retirement horizon doesn’t mean you need to double your savings. In fact, you only need about a 17.5% larger nest egg. This revelation was a "Eureka moment" in my own planning journey, offering reassurance that early retirement is more attainable than many believe.

Historical Resilience

Historically, safe withdrawal rates have survived some of the worst economic downturns, such as the Great Depression and the tumultuous 1960s and 70s. This resilience should offer comfort to those wary of market volatility.

Additional Considerations

Beyond personal savings, early retirees can also benefit from other income streams such as pensions and social security. These supplemental cash flows can significantly boost your financial security and potentially allow for higher withdrawal rates later in retirement.

Case Studies and Examples

In several case studies I've conducted, supplemental income streams like pensions and social security allowed for withdrawal rates to exceed 4% again, even with longer retirement horizons. For instance, a bare-bones retirement might require a 3.5% withdrawal rate, but with additional income, it could rise above 4%.

Final Thoughts

While the prospect of early retirement requires careful planning and potential adjustments to traditional withdrawal strategies, there's good news. Personalized analysis and realistic expectations can reveal higher spending rates than initially anticipated. Despite the need for a slightly larger nest egg, the dream of early retirement remains within reach for many.

Remember, your journey is unique — and with the right tools, data, and mindset, it's absolutely possible to craft a secure and fulfilling retirement that lasts as long as you need it to.

For further reading and a deeper dive into the specifics of withdrawal rates and retirement planning, I recommend checking out my Safe Withdrawal Rate Series, particularly Part 2, which explores the effects of different horizons and asset depletion versus preservation.

Good luck on your journey to early retirement!

Frequently Asked Questions

The 4% rule is a retirement withdrawal guideline stating you can withdraw 4% of your portfolio in year one, then adjust that amount for inflation each year, with a historically high probability of your money lasting at least 30 years.

Research continues to support the 4% rule for 30-year retirement periods, though some financial planners recommend 3.25-3.5% for added safety in today's lower-yield environment, especially for early retirees with longer time horizons.

Multiply your annual expenses by 25. For example, if you spend $40,000 per year, your FI number is $1,000,000. This is because 4% of $1,000,000 = $40,000.

Yes. You withdraw 4% in year one, then increase that dollar amount by inflation each subsequent year. So if you withdraw $40,000 in year one and inflation is 3%, you withdraw $41,200 in year two.

The Trinity Study (1998) analyzed historical stock and bond returns from 1926-1995 and found that a 4% withdrawal rate from a portfolio of 50% stocks and 50% bonds had a 95% success rate over 30-year periods.

Many financial experts recommend early retirees use 3.25-3.5% to account for longer retirement periods (40-60 years). However, early retirees often earn some income, which significantly reduces the actual withdrawal rate needed.

The Bottom Line

The 4% rule remains one of the most useful benchmarks in retirement planning. While it is not perfect, it gives you a clear FI number to target: your annual expenses times 25. For early retirees, build in extra margin with a slightly lower withdrawal rate and flexible spending, and your money has an excellent chance of lasting a lifetime.

Safe withdrawal rate

4%

FI multiplier

25×

Historical success rate (30yr)

95%+

See how the 4% rule applies to your situation with our free FI number calculator.

Model Your Path to Retirement

Project your retirement timeline based on your savings rate and investment returns.

Run the Numbers