Episode Summary

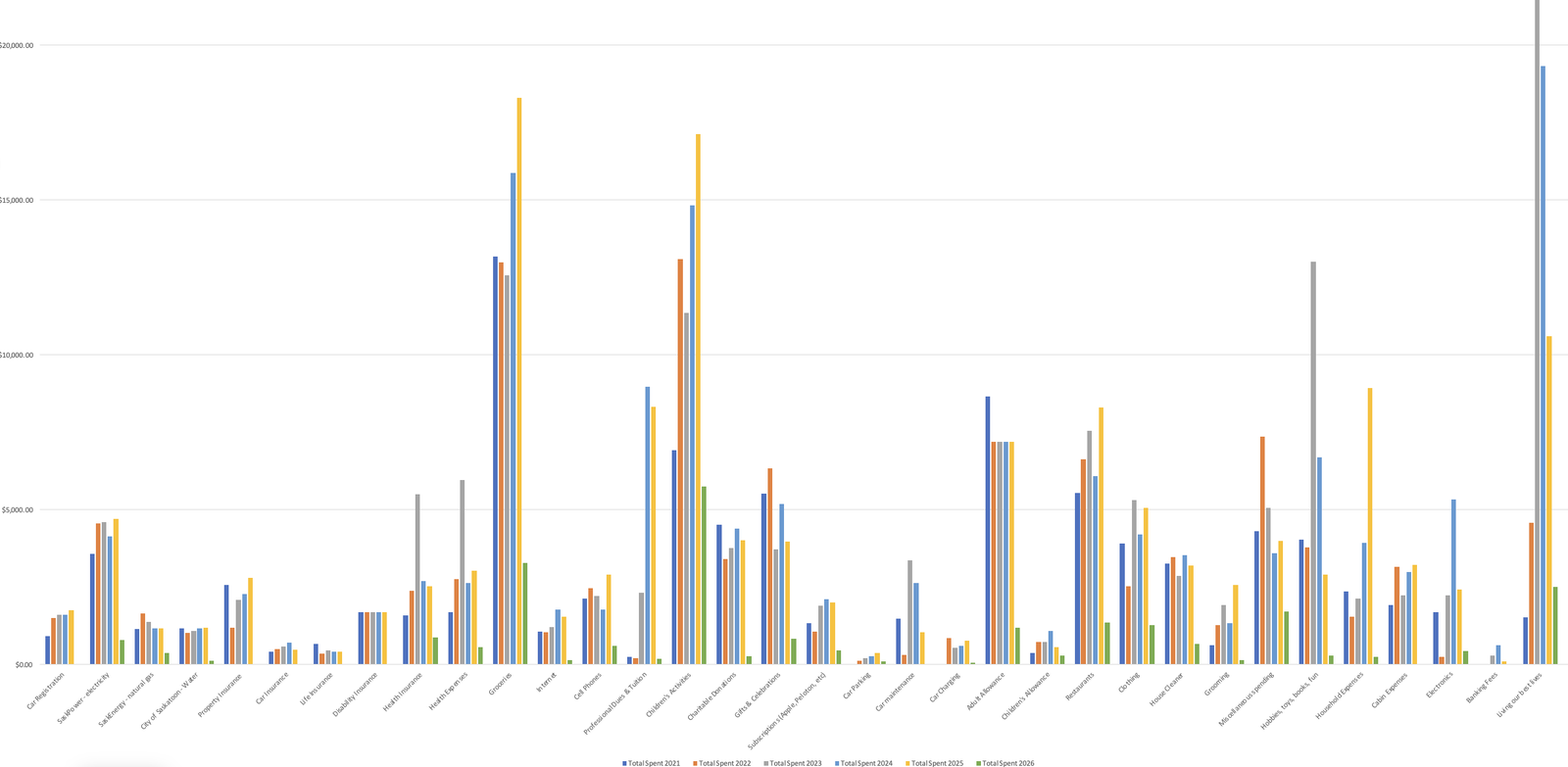

In this episode of ChooseFI, the hosts delve into the concept of an expense audit, encouraging listeners to analyze their spending habits over the past month. They discuss feedback from community members and highlight the value matrix, a tool for categorizing expenses based on joy versus cost. This interactive episode promotes proactive financial management and community engagement as listeners embark on the journey towards financial independence.

Key Tactical Takeaways

- Conduct an Expense Audit: Review your expenses for February to March to identify spending leaks.

- Utilize the Value Matrix: Categorize expenses into high/low joy and high/low cost to optimize spending.

- Regular Check-ins: Establish a routine of auditing and reflecting on your spending habits to refine financial strategies over time.

Core Rules & Formulas

| Rule/Formulas | Description |

|---|---|

| Expense Audit | Evaluate your spending regularly to identify leaks or unnecessary expenditures. |

| Value Matrix | A four-quadrant tool to assess expenses based on joy and cost: |

| - High Joy, Low Cost (Best) | |

| - High Joy, High Cost (Consider optimizing) | |

| - Low Joy, Low Cost (Keep but examine) | |

| - Low Joy, High Cost (Cut or trim) | |

| Save 50% Rule | Aim for a 50% savings rate to ensure financial security and independence. |

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Free FI Planning Tools + Community

FI calculator, expense audit, Coast FI tracker, local groups, and 750+ podcast episodes.

No password needed. Free forever.

Tools, Accounts, or Strategies Mentioned

| Tool/Strategy | Description |

|---|---|

| Expense Audit Challenge | Community initiative to assess spending from February to March. |

| Value Matrix | Tool for analyzing expenses to prioritize spending based on joy and cost. |

| YNAB (You Need A Budget) | Budgeting tool that tracks spending efficiently; useful for expense audits. |

| Monarch Money | Expense tracking tool integrated with financial accounts for easier audits. |

Resources & References

Clear Calls to Action

- Start Your Expense Audit: Begin reviewing your expenses now to uncover potential leaks.

- Engage with the Community: Share your audit findings and strategies on the ChooseFI platform.

- Utilize the Value Matrix: Apply this framework to reflect on your spending and make informed decisions.

- Listen to Episode 586 for more details on initiating your expense audit and understanding its importance.

Top Travel Card

Ready to unlock a world of free travel? Start with the Chase Sapphire Preferred® Card

$95 annual fee | Earn 100,000 bonus points

Best Card for Side Hustlers and Business Owners

Side hustlers! With the Ink Business Preferred® Credit Card you can earn free travel from your business expenses.

$95 annual fee | Earn 100,000 bonus points

Most Flexible Travel Card

The Capital One Venture Rewards Credit Card can be used to offset almost any travel expense.

$95 annual fee | Earn 75,000 Miles once you spend $4,000 on purchases within 3 months from account opening

ChooseFI has partnered with CardRatings for our coverage of credit card products. ChooseFI and CardRatings may receive a commission from card issuers.

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Free FI Planning Tools + Community

FI calculator, expense audit, Coast FI tracker, local groups, and 750+ podcast episodes.

No password needed. Free forever.