Most people chase financial independence through side hustles and raises. Brad and Jonathan flip that equation: audit your expenses first, then watch your FI date accelerate without earning another dollar.

They walk through a structured four-step framework for conducting annual expense audits that help you identify money leaks and understand your true living costs. The discussion covers practical strategies for tracking subscriptions, variable expenses, and distinguishing between required and discretionary spending. By adopting a calculated approach to expenses, you can effectively mitigate lifestyle creep while ensuring every dollar serves a purpose in your budget. The overarching message encourages focusing on building a life of value, emphasizing joy and fulfillment in financial management, rather than mere restriction.

Key Tactical Takeaways

- Conduct an Annual Expense Audit: Establish a routine to review expenses at least once a year to stay on top of spending habits and identify areas for improvement.

- Categorize Every Expense: Break down expenditures into necessary (fixed costs) and discretionary (variable costs) categories for clearer insights.

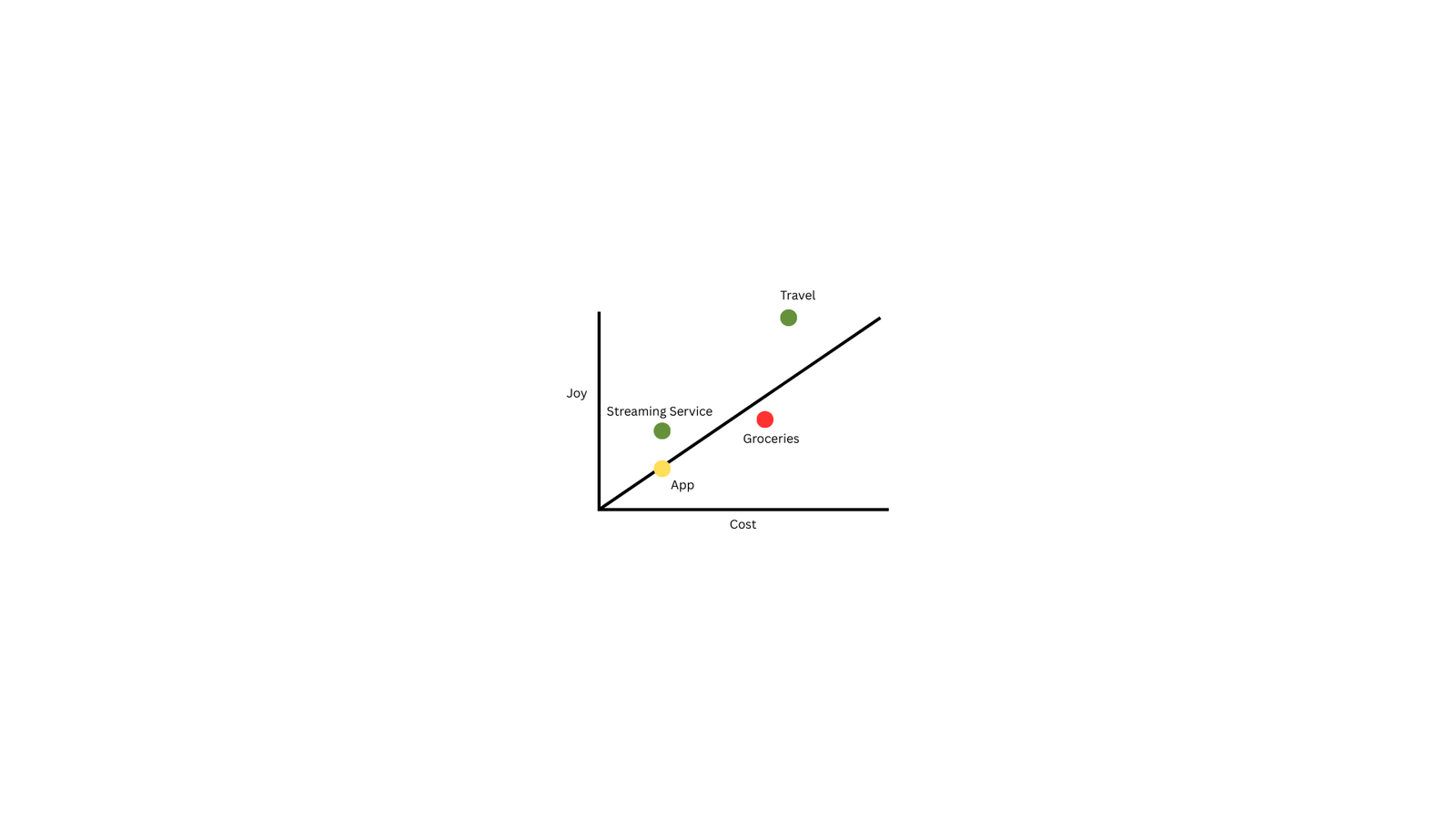

- Use a Value Matrix: Assess expenses based on their joy and necessity to inform which should be retained, reduced, or eliminated.

- Track Subscriptions and Variable Costs: Pay attention to recurring payments, particularly those related to entertainment and services like streaming or software.

- Calculate the Long-Term Impact of Small Savings: Cutting small monthly expenses can significantly affect your financial independence number over time.

Core Rules & Formulas

| Rule | Explanation |

|---|---|

| Annual Expense Audit | Review all expenses once a year to prevent overspending and identify leaks. |

| Categorization of Expenses | Differentiate between Required (fixed) and Discretionary (variable) expenses. |

| Value Matrix Implementation | Organize spending into High Joy/ Low Joy and Essential/ Eliminate quadrants. |

| Prioritize Necessary Expenses | Always account for essential bills, including utilities, groceries, and housing costs. |

| Evaluate Impact of Expenses | Each $100 cut from monthly expenses reduces your FI number by $30,000 over time (20-year horizon). |

Tools, Accounts, or Strategies Mentioned

| Tool/Strategy | Link/Description |

|---|---|

| Expense Audit Spreadsheet | Download here |

| Chase Ultimate Rewards | Utilize for travel rewards and points transfer to hotel partners. |

| Value Matrix Framework | Framework for analyzing the necessity and joy of expenses. |

Key Quotes

"Every dollar must earn its place in your budget." (00:05:23)

"Even the most intentional spenders can lose track of their expenses." (00:06:19)

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Join 25,000+ on the Path to FI

Free access to FI tools, forums, local groups, and 750+ episodes.

No password needed. Free forever.

"Small expenses can add up to significant savings." (00:13:08)

"Have you assessed the true cost of your life?" (00:13:17)

Chapters

- Introduction to Expense Audit (00:00:00)

- Importance of Regular Expense Audits (00:05:23)

- Identifying Money Leaks (00:13:04)

- Key Strategies for Expense Auditing (00:22:34)

- Value Matrix for Expenses (01:03:05)

- Closing Thoughts and Action Steps (01:09:13)

Terminology

Expense Audit: A detailed review of all expenditures to identify unnecessary spending and money leaks. (00:05:23)

Lifestyle Creep: The tendency for expenses to increase as income rises, often leading to a strain on finances. (00:08:11)

Value Matrix: A categorization tool to assess the joy and necessity of expenses, helping prioritize what's essential in your budget. (01:03:05)

Resources & References

- ChooseFI Episode 009: Travel Rewards Framework

- Expense Audit Spreadsheet: Download

Action Items

- Download your bank and credit card statements for the last few months to start your audit. (00:55:06)

- Categorize your expenses into necessary and discretionary for better insights. (01:03:05)

- Join the community challenge to share findings and get support during your expense audit process. (01:09:13)

Top Travel Card

Ready to unlock a world of free travel? Start with the Chase Sapphire Preferred® Card

$95 annual fee | Earn 100,000 bonus points

Best Card for Side Hustlers and Business Owners

Side hustlers! With the Ink Business Preferred® Credit Card you can earn free travel from your business expenses.

$95 annual fee | Earn 100,000 bonus points

Most Flexible Travel Card

The Capital One Venture Rewards Credit Card can be used to offset almost any travel expense.

$95 annual fee | Earn 75,000 Miles once you spend $4,000 on purchases within 3 months from account opening

ChooseFI has partnered with CardRatings for our coverage of credit card products. ChooseFI and CardRatings may receive a commission from card issuers.

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Join 25,000+ on the Path to FI

Free access to FI tools, forums, local groups, and 750+ episodes.

No password needed. Free forever.

My favorite part of the episode was the final discussion on the cost/value matrix, I hadn't really had that idea directly related back to my expense audit before.

My favorite part of the episode was the final discussion on the cost/value matrix, I hadn't really had that idea directly related back to my expense audit before.