Hi Brad, good morning — I’m a bit skeptical of the new 5.5% safe withdrawal rate proposal from Bill Bengen, mostly since it seems to conflict so significantly with Big Ern’s research. Do we know what assumptions Bengen is using to come to this conclusion?

Listen to the Answer

The New Safe Withdrawal Rate: Is It Really Safe?

The personal finance world has been set abuzz by Bill Bengen's latest proposal: a safe withdrawal rate of 5.5%. This recommendation marks a considerable deviation from the time-honored 4% rule, a shift that could, at first glance, appear to be a game-changer for retirees. If proven true, this new rate would indeed represent a "massive improvement in retirement finances," potentially boosting withdrawal capability by a significant margin. Imagine increasing your retirement withdrawals from $40,000 to $55,000 annually on a $1 million portfolio—a 37.5% increase! However, many experts, myself included, are viewing this proposal with skepticism,

I think this is a "big nothing burger." Let's dive into the details and see why.

Model your path to retirement

Test withdrawal strategies and see how long your portfolio lasts.

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Free Coast FI Calculator

Model when you can stop saving and let compound growth carry you to retirement.

No password needed. Free forever.

Understanding the Traditional 4% Rule

Historical Context

The 4% rule is a cornerstone of retirement planning, originating from the seminal research by Bill Bengen and further validated by the Trinity Study. This rule provides a framework for retirees to manage withdrawals in a way that mitigates the risk of outliving their savings. The assumptions underlying the 4% rule are critical to understanding its enduring relevance:

- Investment Horizon: The rule assumes a 30-year retirement period.

- Asset Depletion: There's an acceptance of the possibility of depleting the portfolio.

- Portfolio Composition: Typically, a balanced portfolio with 50-75% equities and the rest in secure U.S. government bonds.

- Withdrawal Strategy: Start with a 4% withdrawal of the initial portfolio value in the first year, adjusting subsequent withdrawals for inflation.

Success Rate

Historically, the 4% rule has been remarkably successful. With only a 1.5% chance of running out of money, this rule boasts a 98.5% success rate of lasting the entire 30 years. These numbers underscore the robustness of the 4% rule in providing a reliable framework for retirement planning.

| Assumptions | 4% Rule | New 5.5% Proposal |

|---|---|---|

| Equity Allocation | 50-75% | 55% (diversified across various sectors) |

| Bonds | Remainder in U.S. 5-year government bonds | 40% U.S. intermediate (10-year) Treasury bonds |

| T-bills | Not specifically included | 5% |

| Initial Withdrawal | 4% of initial portfolio | 5.5% |

For readers interested in the foundational research, the original Trinity Study provides an in-depth look at the historical success rates of various withdrawal strategies. I also recommend my Safe Withdrawal Rate Series.

Bengen's New Proposal: The 5.5% Withdrawal Rate

Step 1: New Asset Allocation

Bengen proposes a significant shift in portfolio composition to support a higher withdrawal rate. This involves moving away from a broad U.S. stock index approach to a more diversified equity allocation, emphasizing small-cap and international stocks. Here is the proposed portfolio structure:

- 55% Equities:

- 11% U.S. large-cap stocks

- 11% U.S. mid-cap stocks

- 11% U.S. small-cap stocks

- 11% U.S. micro-cap stocks

- 11% international stocks

- 40% U.S. Intermediate Treasury Bonds

- 5% T-bills

The rationale here is that this diversified asset allocation, with assets that had historically better returns than the US broad market could theoretically sustain a higher withdrawal rate by capturing returns across various sectors of the stock market. For more details on Bengen's asset allocation changes, you can refer to this MarketWatch article.

Step 2: Changing Success Criteria

Bengen's second step introduces a modification in the criteria for success. He argues that with his new asset allocation, a 4.7% fail-safe rate is achievable, at least for the cohort of retirees in late 1968, who faced significant economic challenges. Additionally, under what Bengen calls "normal conditions," he suggests a withdrawal rate as high as 7% during normal market valuation scenarios, but a more modest 5.5% withdrawal rate to account for the current elevated CAPE Ratio. He suggests a more dynamic approach, adjusting the withdrawal rate based on prevailing economic indicators.

The Skeptic's View: Why the 5.5% Rate May Not Hold

Performance of Small-Cap Stocks

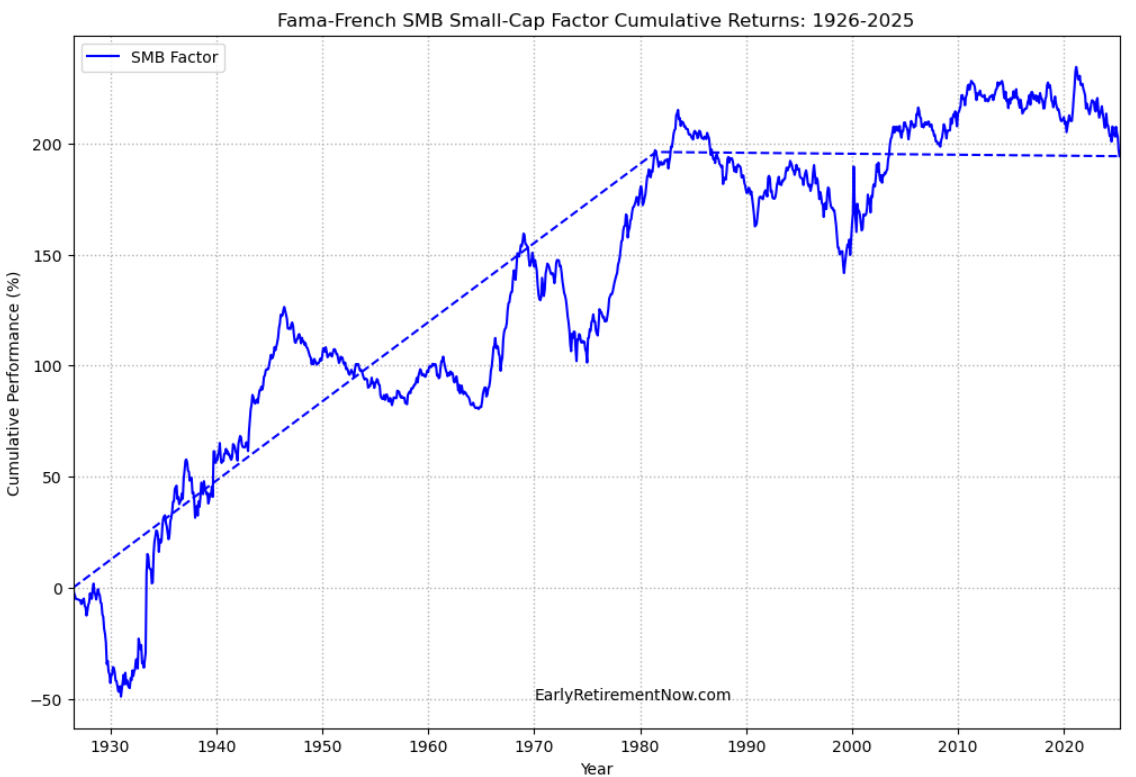

Because Bengen's proposal hinges on the strong historical performance of small-cap stocks, it's essential to scrutinize this assumption. Historically, small-cap stocks outperformed until about 1980, after which their edge diminished significantly or even vanished. See the cumulative return chart, based on the research of economists Eugene Fama and Ken French.

The less profitable small-cap premium since 1980 is largely due to market efficiency, i.e., increased market awareness and participation. This reality challenges the reliance on small-cap stocks to significantly boost withdrawal rates for today's retirees. For a deeper exploration of these dynamics, see Part 62 of my Safe Withdrawal Rate series.

Critique of the New Criteria

Bengen's use of an average withdrawal rate rather than a fail-safe one introduces potential pitfalls. The average withdrawal rate, by nature, offers safety only "on average," meaning it inherently carries a higher risk of failure — possibly over 50% in some scenarios. I want to stress the danger of portraying an average rate as a safe one, a point that has unfortunately been glossed over by many media outlets eager for a sensational headline.

Final Thoughts: Sticking with the 4% Rule

In conclusion, Bengen's 5.5% proposal, while intriguing, does not hold up as a truly safe withdrawal rate. The 5.5% figure is better described as an average withdrawal rate, carrying a significant risk of financial shortfall over a 30-year period. It also relies on the Small-Cap Premium to exit its 45-year slumber. In contrast, the tried-and-true 4% rule remains a more reliable strategy, offering retirees the peace of mind of a high success rate with minimal risk of outliving their savings.

Despite the allure of a higher withdrawal rate, the financial implications of shifting away from a battle-tested strategy are considerable. The 4% rule's robustness in providing financial security for retirees remains unmatched, particularly in an age where market efficiencies have eroded many of the historical advantages once captured by niche investment strategies.

I encourage retirees and planners alike to approach the 5.5% proposal with caution and to consider the underlying risks associated with such a significant departure from established wisdom. For those interested in exploring customized withdrawal strategies, tools like my new online calculator Safe Retirement Spending can provide insights into how different scenarios might affect your retirement outlook.

Risks of the 5.5% Proposal

- Higher Risk of Failure: An average, not a fail-safe.

- Relying on Historical Small-Cap Performance: No longer as advantageous.

- Dynamic Adjustments: Complexity and uncertainty in execution.

- Potential for Financial Shortfall: Especially critical for longer retirement horizons.

With these considerations in mind, I wish you the best in your retirement planning journey. Stick with strategies that prioritize safety and sustainability, and thank you, Mike, for sparking this critical discussion.

Model Your Path to Retirement

Project your retirement timeline based on your savings rate and investment returns.

Run the Numbers